Publications

Publications

Partners

Partners

Guaranteed life annuities are considered old-school, but an actuarial analysis shows they may be the best option for most retirees, writes Jeanine Astrup.

- For more financial news, go to the News24 Business front page.

At retirement, the journey towards picking an annuity product that will turn your savings into a regular income for as long as you live is often fraught with frustration and anxiety.

While you have three choices at retirement - a guaranteed life annuity, a living annuity, or a combination of both – you just don’t know what you don’t know. This can make it difficult to ask the right questions to help you make the best choice for your circumstances.

If you turn to Google for help, you’ll be forgiven for thinking that a living annuity is the only sensible option when you retire. After all, a living annuity allows you to pick the underlying investments, adjust income drawdown levels once a year, and bequeath any leftover capital to your beneficiaries.

Guaranteed life annuities, on the other hand, are considered old-school, mainly because it is difficult to source a complete comparison of annuity rates and examples of how much income you can buy with your investments.

You have to speak to a financial advisor for this, whereas you can get a good feel for the benefits of living annuities by doing online research.

Capital legacy versus income legacy

Even if a consumer understands the difference between a living annuity and a guaranteed life annuity, most are put off by the fact that once the guaranteed life annuity has been bought, the capital sum is converted to income, and this cannot be reversed.

The implication is that when the annuitant dies, no lump sum benefit can be paid to beneficiaries. As a result, a general misconception is that when you die, your money dies with you.

There are, however, options that will ensure your money does not die with you. With a guaranteed life annuity, you can leave an income legacy by adding a dependant who will continue receiving an income once you die for a guaranteed period or life. However, it is important to understand that these options come at a cost and will reduce the income you receive during your lifetime.

Most pensioners opt for a living annuity and sacrifice the certainty of a lifetime guaranteed income in the hope that some capital will remain for a loved one when they die. The outcome for some is that the capital is whittled away before they die, leaving them with no income and family members to inherit the financial burden of supporting their ageing loved ones.

What the numbers say

Having crunched the numbers, it is clear most retirees would be better off buying guaranteed life annuities or a hybrid solution (a combination of a guaranteed life and a living annuity).

This is especially true in the current environment where guaranteed life annuity rates are at levels last seen more than 10 years ago. This represents an incredible opportunity if you are retiring!

The benefits of a living annuity only really apply to the wealthy, to people with advanced financial skills, to people with expenses well below a sustainable living annuity income, or those with a short life expectancy due to illness. It is a very sophisticated financial instrument with an enormous burden to manage.

Retiring with R1 million

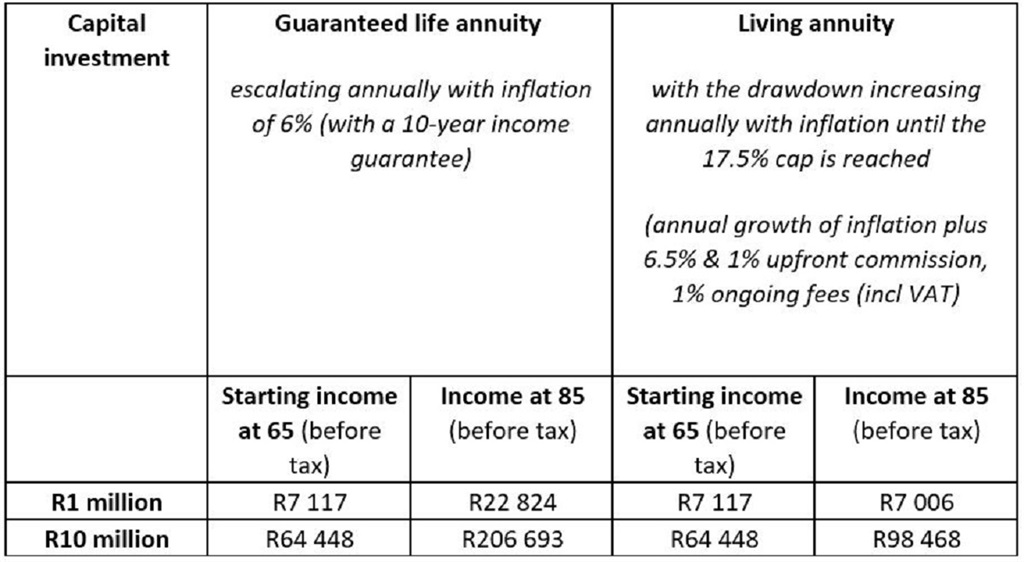

Take the single male who is 65 years old and has saved R1 million for his retirement. He decides to buy a guaranteed life annuity with a 10-year guarantee because he would like to leave something for his daughter should he die before he turns 75. He would like his pension to keep pace with inflation and therefore opts for a guaranteed life annuity that increases with inflation every year.

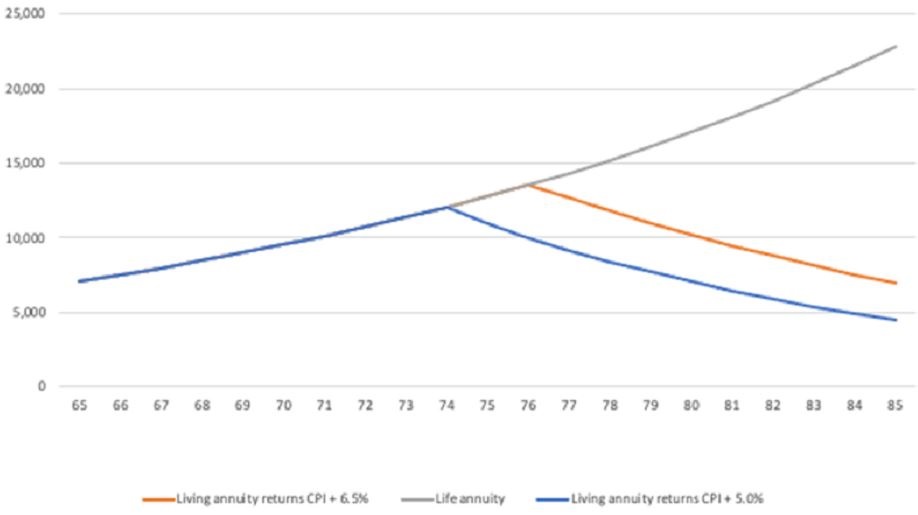

Our calculations show his starting pension (before tax) is R7 117. By the time he turns 85, his monthly pre-tax income will have increased with expected inflation of 6% to R22 824 and will continue to increase yearly until he dies, even if he lives to 100 and beyond.

A living annuity investment, on the other hand, would have wiped out a significant portion of the R1 million invested over the 20 years if he had opted for a starting pre-tax income of R7 117 a month, requiring a drawdown rate of 8.54%.

Assuming that the living annuity pension increases with inflation each year until it reaches the living annuity drawdown cap of 17.5%, this pensioner would be left with a monthly income of just R7 006 by the time he turns 85. The calculations assumed a very optimistic investment growth of inflation plus 6.5% and 1% upfront commission and 1% ongoing fees (inclusive of VAT).

The graph below illustrates the long-term income pattern achieved by an investment of R1 million in a guaranteed life annuity versus a living annuity with a return of inflation plus 6.5% and a living annuity with a return of inflation plus 5%.

Assumptions: A single male aged 65, R1 million investment, living annuity fees (1% upfront commission and 1% ongoing fees). Income increases with inflation every year.

Retiring with a lump sum of R10 million

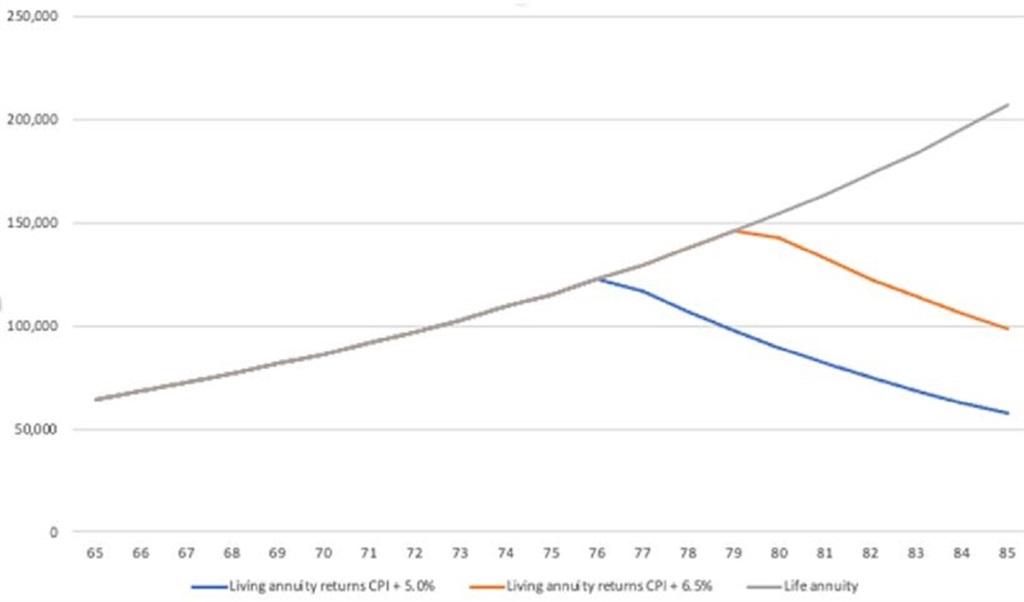

For most South Africans, a retirement nest egg of R10 million is unachievable. Nevertheless, crunching the numbers highlight the benefits of a guaranteed life annuity, even if you are retiring with sizeable retirement savings of R10 million, again using the example of a single male aged 65.The cost of the guaranteed life annuity is influenced by the size of the income required, which means the bigger the pension, the higher the cost.

Therefore, a guaranteed life annuity of R10 million with a 10-year guarantee will buy a monthly income of R64 448, which increases with expected inflation of 6% every year until the owner dies. By the time he reaches age 85, his monthly pre-tax income will be R206 693, assuming inflation of 6% each year.

To achieve the same starting income with a living annuity, a drawdown rate of 7.73% is required. If the portfolio achieves annual investment growth of inflation plus 6.5%, his income will peak at R145 710 at age 79 and then decline. At age 85, his income would be R98 468, less than half of what the guaranteed life annuity would be paying. The chart below illustrates this.

Assumptions: A single male aged 65, R10 million investment, living annuity fees (1% upfront commission and 1% ongoing fees). Income increases with inflation every year.

Case studies in summary

Consider all options

With current annuity rates at such a high level, R1 million can buy a male pensioner a non-increasing monthly pension of almost R11 000 guaranteed for life. Women generally qualify for a lower monthly income than men because their life expectancy is higher.

While we don’t recommend annuities that do not increase with inflation because you would not be protected against future cost increases, there is an opportunity to combine guaranteed life annuities and living annuities to achieve a higher starting pension without risking the complete erosion of capital.

The role of a trusted financial advisor is invaluable when it comes to picking the right vehicle designed to turn your retirement savings into a reliable income stream during retirement.

If you detect a bias for living annuities and are not presented with calculations that present an overview of all options, including a hybrid solution, consider getting a second opinion from another financial advisor.

Before you make your final decision, consider the following:

- Discuss your options with your family and get their buy-in. You may find that your loved ones would gladly forego a potential inheritance for the security that comes with you having a guaranteed income for life that keeps pace with inflation.

- If you are gravely ill and your life expectancy is short, a living annuity is likely to be a better option for you.

- A combination of a guaranteed life annuity and a living annuity (hybrid annuity) could be a good solution, even if you retire with a sizeable nest egg.

- Guaranteed life annuities can be structured in several different ways to allow for spouse’s pensions and a lump sum payout to beneficiaries if you die during a guarantee period.

- Speak to a trusted financial advisor and ensure you are presented with calculations that illustrate the outcomes of all options (guaranteed life annuity, living annuity and a hybrid solution), not just a living annuity.

- If you opt for a living annuity, consider the ongoing requirement to make decisions regarding underlying investments and the draw-down rate. Initially, this may not seem like a burden, but as you get older, the process may become more challenging and the financial advisor who first helped you may no longer be around.

- As you age, the risk of dementia increases, which may result in poor investment decisions. Having a base level of guaranteed income for life mitigates these risks.

Jeanine Astrup is a consulting actuary and member of the Actuarial Society of South Africa (ASSA) Retirement Matters Committee.

News24 encourages freedom of speech and the expression of diverse views. The views of columnists published on News24 are therefore their own and do not necessarily represent the views of News24.